Are you considering buying a final expense insurance policy with guaranteed acceptance? You have taken a great step in securing your beneficiaries from the hassles of bearing your funeral costs. Instead of them shelling money out of their pocket for your funeral and other expenses you may leave behind after you depart, your insurance will cover such expenses.

Insurance agents like Gary P. Cubeta from “Insurance for final expenses” will help you understand the guaranteed acceptance policies in the market offered by platforms like John Hancock final expense.

With a gamut of policies and procedures, you probably were attracted to the idea of keeping your health history confidential. Or maybe the policy was recommended by a friend, or you may think it’s your only option.

However, before you proceed to sign the dotted line, there’s much to know about final expense insurance with guaranteed acceptance.

What is a Guaranteed Acceptance Final Expense Insurance Policy?

Simply put, guaranteed acceptance is a type of insurance that has no medical underwriting whatsoever. The insurance company is happy to accept you without being aware of a single detail about your health as long as you fulfill simple eligibility requirements like your state of residence and age.

Unlike other types of final expense insurance policies that tend to pry on your lifestyle by asking certain health-related questions or subjecting you to a medical exam, guaranteed acceptance does not have such conditions.

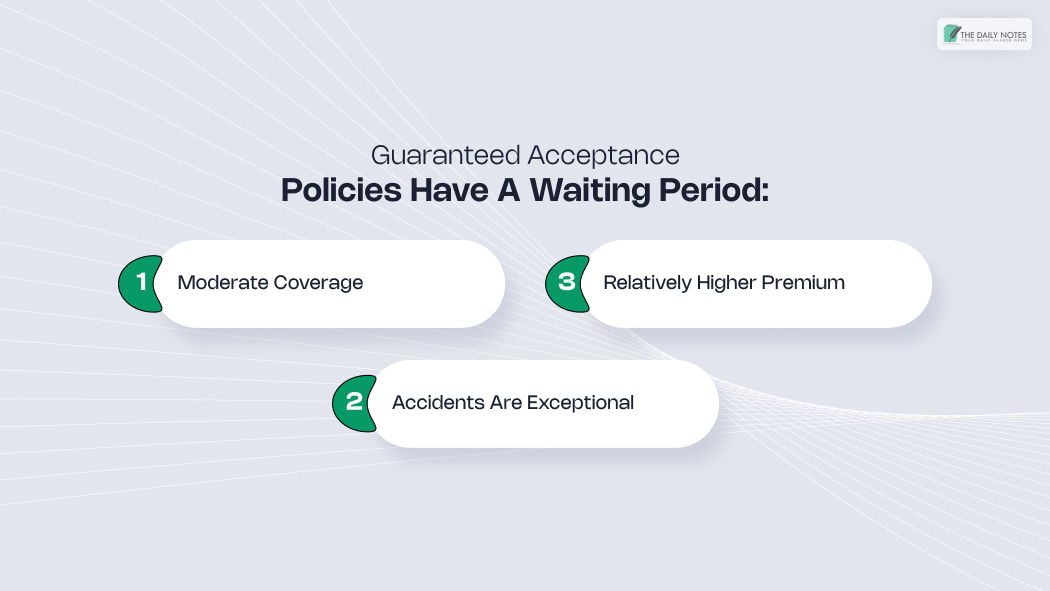

Guaranteed Acceptance Policies Have a Waiting Period:

Before you consider getting a guaranteed acceptance policy, it’s vital to know that these policies come with a waiting period before you can reap their benefits.

Most policies, including policies from providers like John Hancock’s final expense policy, have a two-year waiting period in which you cannot make any claims.

Hence, if you depart during this period, you may not get complete coverage or a death benefit. However, your beneficiaries will still get a refund of the premium paid along with any accrued interest rate of 10%.

Only after the waiting period has ended you can avail yourself of death benefits. Insurance companies mandate this waiting period to reduce their risk propositions.

Here are some important features of a guaranteed acceptance policy you need to be aware of:

Moderate Coverage –

As this policy attracts seniors with serious health conditions, apart from the 2-year waiting period to mitigate the risk proposition, the policies also tend to have moderate coverage. Typically you can opt for coverage up to a maximum of $25,000.

Relatively Higher Premium –

Most guaranteed acceptance policies have a substantially higher price tag compared to policies with medical underwriting.

Accidents are Exceptional –

Even though you will not get any death benefit during the waiting period, the only exception is if you pass away due to an accident. In such a case, your beneficiaries may still get full benefits, even during the waiting period.

When is Guaranteed Acceptance Final Expense Policy a Good Buy?

If you are likely to qualify for final expense policies with an underwriting process, you don’t have to default to a guaranteed acceptance policy. However, there are certain circumstances where it might be a good option for some:

1. Only Option Due to Your Health –

Other types of final expense policies require you to answer a set of health questions, and if you don’t qualify, they might not accept you. These conditions are known as knockout conditions:

- Terminal illness with a life expectancy of under 24 months

- Undergone any organ or tissue transplant

- Currently on dialysis

- AIDS or HIV

- Diagnosed with Cancer, Alzheimer’s, or Dementia

- In a nursing home or receiving Hospice care

2. Cheapest Option Because of your Health –

Certain health conditions are considered high-risk and may attract a higher premium rate than other types of final expense policies. If the medical underwriting process of policies puts you in a higher risk category, it may warrant a higher price.

3. Personal Preference

Some individuals prefer privacy and don’t want to reveal their medical history to third parties. In such conditions, it may be convenient to opt for a guaranteed issue policy.

The smaller coverage amount that is typically offered by final expense insurance in comparison to traditional life insurance makes it a great option.

You can expect a range of $ 5000 to $ 25000. This is primarily to cover funeral-related costs which can fall anywhere between $7000 to $12000 in the country.

Pure medical exams and health questions in comparison to traditional Life insurance make it easier to qualify.

In addition, many insurance providers guarantee acceptance which means applicants do not have to fear rejection due to their health condition or age.

The Bottom Line:

In general, it’s best to go for guaranteed acceptance policies like John Hancock’s final expense if you are unable to qualify for a policy that has underwriting and if you prefer not revealing your medical history. A guaranteed acceptance policy comes with a greater waiting period and a higher premium. Therefore you need to know what you are signing up for before you apply for one.

Thus, explore your options for various final expense policies to understand whether they fulfill your requirements in your best interests.

Consult a top independent insurance agent to compare different policies according to your medical conditions and age and make a sensible decision before signing the dotted line.

Read Also: